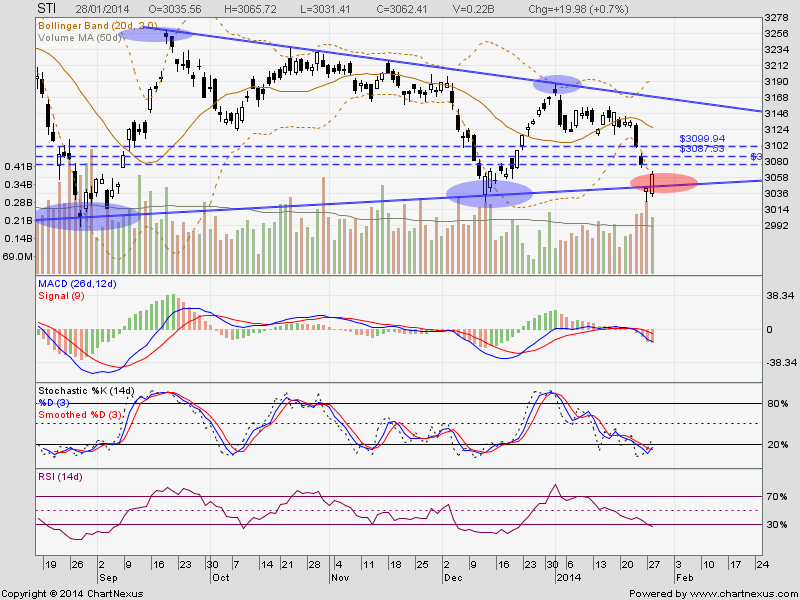

STI broke an important support of 3242. It also broke the 200 MA today. Will support 3187 hold?

Take a look at the monthly chart. It may be forming double top, with declining volume on the right shoulder

Well, this might not be such a good topic to discuss about, especially it is going to be Chinese New Year soon. But this question kept me in suspense for a long time. Today, I did some research on the internet. It seems this topic is under Estate Planning. I have a few questions. What will happen to my monies in:

I extracted the information from Singapore Estate Planning Services. Please check out their website for details.

The surviving joint account holder should provide the bank with a copy of the death certificate, and bring proof of identity (e.g. NRIC) to close the account. The bank will usually automatically give the account balance to the surviving account holder once the account is closed. This is provided the joint account is not pledged to a liability of the bank (e.g. overdraft, or business capital facility).

If there is more than one surviving joint account holder, the bank will usually proportionally allocate the balance. In this case, all parties must be present and provide the relevant documentation to close the account and withdraw the money. If there is any dispute over the allocation, the bank can freeze the account and advice the surviving account holders to seek a court order to settle the dispute.

If the fixed deposit or savings account is held in a single name, the family members or the legal representative can apply for release of funds from the bank. The degree of complexity depends on the amount. By and large, banks prefer to deal with the legal representative of the deceased person’s estate with the appropriate a letter of administration or grant of probate.

If the amount is less than $5,000, the deceased “next-of-kin” (claimant) can approach the bank without a letter of administration or grant of probate. Next-of-kin is restricted to the following:

[Source: http://www.estateplanning.com.sg/estate-settlement-process-of-bank-account/]

Upon knowing that the investor has died, the deceased person’s securities account will be updated to an estate account. The personal representative of the estate needs to extract a letter of administration or a grant of probate from the court, and present it to CDP in person. The other documents needed are the death certificate, asset schedule, and the personal representative identification card. Subsequently, a request to transfer the securities can be made.

It is not necessary to liquidate the securities. These securities can be transferred to the rightful beneficiaries according to the deceased person’s will or under the intestacy law. The personal representative will be notified once the transfers are completed.

There will be a transfer fee incurred. At the time of this writing, the fee is $10.70 (inclusive of GST) per counter per transfer request.

If the grant of probate is extracted overseas, the foreign grant has to be resealed in Singapore Court.

If the personal representative is overseas, his signature has to be witnessed by the Notary Public, and the supporting documents have to be certified by the Notary Public before mailing to CDP.

[Source: http://www.estateplanning.com.sg/estate-settlement-of-equity-and-bond/]

If the property is in sole ownership of the deceased without mortgage, the legal representative could transfer the ownership according to the will or the Intestacy laws (if there is no will). Alternatively, the property could be sold and the proceeds be distributed amongst the beneficiaries.

During the estate settlement of property process, the legal representative needs to be mindful that there will be property up-keeping costs involved. These include a property tax, property management & sinking fund, utility bills, insurance etc. These costs should be paid by the estate account.

If you are a Muslim, you need to give serious thought to the sole ownership of your matrimonial property. Because upon your death, your legal representative would most likely sell the property and distribute the proceeds according to the Faraid (Muslim Intestacy Law). Your surviving spouse could end up without a home.

This is the most common form of property ownership in Singapore, especially amongst husband and wife. In legal language, this is known as “joint tenancy”. The title deed will state the co-owners hold the property as “joint tenants”. In a joint ownership, there is a single title, interest, time of commencement of title, and unity of possession. These are known as the 4 unities.

When a joint-owner dies, his right is extinguished and vested in the surviving joint-owner(s) until the last surviving owner becomes the sole owner of the property. This is the unique feature of joint tenancy which is commonly known as the “right of survivorship”. The joint owner is legally incapable of transferring (or gifting) his joint interest in the property by will to others. On his death, his property interest will pass to the surviving joint owner(s) automatically.

If there is an intention to give one’s share to another, the joint tenancy can be unilaterally severed. Agreement from the other joint owner is not required, but the joint owner will be informed (Section 53(5) of Land Titles Act). This is most applicable in an estate planning situation when 2 parties are going through separation leading to a divorce.

The other co-ownership structure is “Tenancy in Common”, where each co-owner has a separate title and interest in the property, but the shares may vary according to the co-owner’s contribution. This form of property ownership is popular when 2 or more people pool their funds together to co-own a property for investment purposes; or business partners co-own a commercial property. Usually the owners have no legal relationships with each other, unlike a husband and a wife.

The co-owners have an undivided possession of the property. Unlike joint ownership, tenancy in common has no right of survivorship. Upon the death of a co-owner, the deceased person’s share passes to the persons named in his will, or, in the absence of a will, according to intestacy laws.

Therefore, in the estate settlement of a property under tenancy in common, the legal representative could call in the deceased person’s share of the property and distribute it accordingly without the need of agreement from existing co-owners.

Assuming Peter needs to purchase a property, XYZ, without which Jane will not agree to a marriage with Peter. Peter approaches ABC Bank for a mortgage on XYZ property. A mortgage would mean Peter (the borrower, also known as the mortgagor) transfers XYZ property to ABC Bank (the lender, also known as the mortgagee) as a security for the repayment of a $1M loan (also known as a mortgagee loan).

When a bank lends money to a borrower to enable him to buy a property, the main term of the loan is that the borrower will execute a legal mortgage of the property to the bank to secure the repayment of the loan. The legal mortgage is created by a registered transfer of the legal ownership of the property from the mortgagor (borrower) to the mortgagee (lender), subject to the mortgagor’s right to redeem the mortgage.

Therefore, if the borrower dies before discharging the mortgage, the lender (i.e. bank) has the legal ownership of the property instead of the deceased person’s estate. If there is insufficient cash from the estate to settle the outstanding loan, the bank has every right to force sell the property. In this situation, the deceased family members could be left without a home.

The problem could be magnified if the deceased has not one, but two or three mortgages (a common situation especially for property investors), the legal representative has to prioritise the limited liquidity within the estate to resolve the issue.

[Source: http://www.estateplanning.com.sg/estate-settlement-of-property/]

If, at the time of the death, there is no person nominated, the total amount payable shall be paid to the Public Trustee for disposal in accordance with the Intestate Succession Act. If the deceased is a Muslim, the Public Trustee will dispose the Fund according to the Certificate of Inheritance, which the family can obtain from the Syariah Court.

If the nominated person (other than a widow) is below the age of 18 at the time of payment of the amount payable out of the Fund, his portion of the amount payable shall similarly be paid to the Public Trustee for the benefit of the nominated person.

CPF nomination covers your CPF ordinary account, special account, retirement account, medisave account, discounted SingTel shares, and CPF Life annuity. Investment products bought through CPFIS and Dependent Protection Scheme (DPS) Insurance are not covered under CPF nomination. These assets will form part of your estate distributable under a will or Intestate Succession Act.

[Source: http://www.estateplanning.com.sg/estate-settlement-process-of-cpf/]

There a lots more information from their website. Do check it out.

Although the STI chart breakout of the formation (slightly), it did indeed rebounded up, after forming a white hammer near the support line. The rebound is confirmed by the white long candle today. Now, lets watch if the STI can break above the resistance level of 3076. There is also another gap resistance at 3087 – 3099.

Lets look at the indicators:

Bollinger Band: STI is out of band, so there will be tendency to go back to normal (within the band)

MaCD: MaCD line is still below zero line and the bars are still all red. Waiting for one Green to form 4R1G.

RSI: The RSI line is below 30%, over-sold region.

Stochastic: A bullish cross-over in the over-sold region.

Therefore, I think there is a likelihood that STI might be able to rebound past the resistance level.

Recently, when I am looking to switch my housing loan, I was warned about the TDSR. With this framework, many of us might not be able to do a housing loan re-finance as what we have borrowed from bank is based on low interest rate and Debt Servicing Ratio. I did a research and found two posting very informative as they summarize the main points:

“The Monetary Authority of Singapore (MAS) introduced the Total Debt Servicing Ratio (TDSR) framework for all property loans granted by financial institutions (FIs), with effect from 29 June 2013.

In for the kill

Computations of the TDSR affects properties that are residential or non-residential, owned individuals or companies, new applications or re-financed loans, and in or outside Singapore. Declaration and calculation of incomes and loans are also now very detailed.

TDSR may be a new term, with explanations in the FAQs of the TDSR unnecessarily long and difficult to read, but they are only additional sub-clauses to address the loopholes of the Loan-to-Value (LTV) limits announced in the previous property cooling measures.

It is also nothing new to see the government once again adopting a “reactive intervention” approach – dispatch general guidelines to the market, then await speculators to circumvent the loopholes, before sending more stringent rules in for the kill.

What are the killers?

There are four major “killers” in the TDSR framework:

1) 60% threshold

Total debt obligations cannot exceed 60% of total income.

2) 30% haircut

There is an arbitrary 30% cut of all variable and rental income, and 30% to 70% cut for the value of eligible financial assets.

3) 3.5% or 4.5% interest rate

Calculate new loan repayments based on medium-term interest rate of 3.5% for residential properties and 4.5% for non-residential properties, or prevailing interest rate, whichever is higher.

4) Income-weighted average age

If a borrower can’t meet the TSDR threshold, the guarantor will be the co-borrower.

Use income-weighted average age of borrowers rather than younger borrower’s age to determine loan tenure.

Who are the targets?

It is clear that the TDSR is meant to target three main groups of property buyers:

1) Marginal Buyers

Buyers who are highly leveraged with property or non-property debts, and buyers whose affordability depends on low interest rates and betting that it won’t go up too fast too soon

2) Multiple Property Buyers

Buyers who are buying their second, third or more properties with high outstanding loans, and buyers who bought properties recently at a high price, with low rental returns.

Note: Once interest rates go up, owners of multiple properties may not be able to refinance or repackage to lower monthly repayment even for the loan of their own residence if they exceed the TDSR threshold.

3) Two generation buyers

Buyers hoping to benefit from a longer loan tenure by putting the loan under a younger joint applicant’s name, and multiple property buyers hoping to benefit from higher LTV with a joint applicant buying for the first time

Message to parents: it’s time we stopped loaning loans on the next generation.

Work that kills

1) Bonus or commission-based jobs

With a 30% cut on variable income, “salarymen” relying heavily on bonus or commission will be at a disadvantage. For instance, salespeople who have the majority or all of their income based on commissions, or senior executives who have a high proportion of their income based on bonuses.

2) Self-employed, unemployed and retirees

They have to declare all their eligible liquid assets or other assets, amortize the value over four years, and decide whether they will be pledged or not for four years.

3) Staff working in mortgage departments

FIs are required to compute the borrowers’ TDSR with a mountain of information:

– Monthly repayments of all property and non-property debt obligations;

– Gross, variable and rental income after haircut; and

– Eligible assets declared with or without pledge.

And all declarations and supporting documents have to be obtained from applicants and validated with relevant parties. Deviations are not allowed since all exceptions have to be granted by the FI’s board of directors and credit committee.

The 60% threshold is just a start to get FIs familiar with the computation of TDSR. The LTV limits are also not permanent. They are to be reviewed over time and revised at any time. That means all calculations are only temporary and may be required to redo all over again.

Imagine the tremendous amount of extra workload added on the housing mortgage department!

4) Housing loan applicants

Before the TDSR rule, housing loan applicants normally take one week to obtain an approval-in-principal. With the new computation of TDSR, applying for a housing loan is now a long and tedious process.

It is a toil to submit details and proof for all property and non-property debt obligations, variable income and eligible financial assets.

Should owners ask tenants to renew their lease well in advance to ensure that the tenancy agreement has a remaining rental period of at least six months?

Should non-property debt loans include, apart from car loans, renovation loans, student loans and credit card loans, all other purchases paid by installment like electrical appliances, overseas holidays, spa and beauty packages?

Going through all these hassles is the last straw that kills! ”

[Source: http://sg.news.yahoo.com/total-debt-servicing-ratio-kill-101509030.html]

The Total Debt Servicing Ratio (TDSR) framework is to ensure borrowers aren’t overleveraged (i.e. borrowing like a broke alcoholic in a liquor store). It’s a standard that applies to property loans granted by all financial institutions (FIs)*.

*FIs are not always banks.

TDSR calculates the percentage of your income that can go into servicing your loan. At present, the highest TDSR that FIs are meant to allow is 60%.

That means your housing loan repayments, after adding all your repayment obligations (student loans, credit card debts, car loans, personal loans, etc.), cannot exceed 60% of your income.

You may know the terms Debt Servicing Ratio (DSR) and Mortgage Servicing Ratio (MSR), which seem similar to TDSR. They’re not.

MSR only takes into account your housing loan repayments. So a MSR of 30% means 30% of your monthly income can go into home loan repayments, regardless of what your other repayment obligations are.

Then we have the old standard, DSR. And this is where a lot of you will yell (1) “But DSR already factored in all my debts”, and (2) “Wait a second, 60% TDSR is even more relaxed than the old 50% DSR”.

Wrong on both counts.

(1) DSR didn’t factor in certain unsecured loans, such as credit card debt, and

(2) TDSR is more restrictive than DSR. The method for determining your monthly income and loan repayments are different, as we’ll describe below. Also, the range of debts factored into TDSR are much wider.

There’s more to it than that. I’ll explain these effects as we go along:

If you already have an outstanding home loan (or two), it’s unlikely you can take on another without breaking the 60% TDSR.

Of course, it depends on how high your outstanding home loans are. The point is not so much to prevent you buying (although that’s a partial goal), but to ensure you buy only within your means.

Home loans are subject to changing interest rates. So when you take such a loan, the bank doesn’t just use the current rate; they implement a “stress test”, to see if you can handle sudden spikes in interest.

This “stress test” is now standardized at 3.5% for residential properties, and 4.5% for commercial properties.

In other words, home buyers must maintain a TDSR of 60% or under, even if interest rates were to rise to 3.5% (currently, it hovers around 1.7%).

This significantly affects the loan quantum (i.e. the total amount that can be borrowed), even if there’s no outstanding debts.

This is the risk that you won’t be able to refinance into a cheaper loan.

Most home loan interest rates are low for three years, and then go bonkers on the fourth. It’s not impossible to see hikes of one full percent.

At this point, it is (or was) standard practice to switch to another home loan package, with a lower interest rate.

The problem is, a lot of home buyers took their loan packages before the TDSR framework. It was easier to get bigger loans back then.

Should they try to refinance now, they might find they don’t meet the 60% TDSR. These unfortunate people are stuck with their overpriced home loans.

Okay, so TDSR is 60% of your income. But how do you define that income? Not everyone gets a fixed paycheck.

A businessman takes out variable sums from his business, landlords get rent, and salesmen have commissions.

Under the new TDSR framework, that’s lumped under variable income. And FIs are to treat that variable income as though it’s 30% less than it actually is.

So if you’re a business owner making $5,000 a month, your income when calculating your TDSR is just $3,500. That, in turn, means a much lower loan quantum.

Previously, you could stretch your loan tenure by making a joint application with a younger borrower (say, your son).

FIs would just use the age of the youngest applicant. That helped, because a 25 year old can get a 30 year loan tenure, which a 55 year old obviously can’t.

But now, the average age of the borrowers will be used; so a 25 year old and a 55 year old would count as having the collective age of 40.

Also, FIs will only count borrowers with an income. So you can’t be earning nothing, but list yourself as a co-borrower with mum or dad to lower the average age.

What statements do the banks need now? All the statements.

Credit card debts, commissions, student loans, gym memberships, the personal loan you took out to buy a decent Magic deck, all of it. And if you have variable income, you need documentary proof of rent you collect, commissions, fees from clients, etc.

This causes severe complications (e.g. if your clients are in arrears but have collateral, do their fees still count toward your variable income? What about credit cards, if you purposely just pay $50 and not $500 a month?)

For property owners

1. Residential Properties (HDB Flats, Condominiums, Apartments, Bungalows…)

| Scenarios | Types of Property Tax Concession & Relief available |

|---|---|

| Live in your own house | Concessionary Property Tax Rates for Owner-Occupied Residential Properties

|

| Property is unable to be rented out or property is undergoing repairs to make it fit for occupation | [Ceased with effect from 1 Jan 2014]You are trying to rent out your property (Full Vacancy Claim)

|

| Building works on your house (Addition/ Alteration/ Improvement work) | [Ceased with effect from 1 Jan 2014]Property Tax Remission for Residential Property undergoing addition & alteration work (Bldg Work Remission)

|

| Demolition and reconstruction of your house | Property Tax Remission for Residential Property undergoing reconstruction (Bldg-Land Remission)

|

| 2013 Property Tax Rebate for Owner-Occupied HDB Flats | Owner-Occupied HDB FlatsProperty tax rebate to owners of owner-occupied HDB flats for year 2013 |

| 2012 Property Tax Rebate for Owner-Occupied HDB Flats | Owner-Occupied HDB FlatsProperty tax rebate to owners of owner-occupied HDB flats for year 2012 |

| Rebates for owner-occupied homes (ended on 31 Dec 2010) | GST Rebate

2010 Rebate for Owner-Occupied HDB Flats (Owner-Occupied HDB Rebate)

|

| Rebates for owner-occupied homes (ended on 31 Dec 2009) | 2009 Property Tax Rebate for Owner-Occupied Residential Properties (Owner Concession Rebate)

2008 & 2009 Property Tax Rebate (Property Tax Rebate)

|

Please note that all rebates given are on a pro-rated basis according to the actual eligibility period.

[Source: http://www.iras.gov.sg/irashome/page.aspx?id=12158]

Property tax is payable at 10% of the Annual Value (AV) regardless of whether the property is let out, vacant or occupied. Owner occupiers of residential properties may pay concessionary owner-occupier tax rates based on the Annual Values (AVs) of your building as follows:

| Annual Value ($) | Tax Rate (%) |

|---|---|

| First 6,000 | 0 |

| Next 59,000 | 4 |

| Amount exceeding 65,000 | 6 |

Computation of Tax Payable

| Annual Value ($) | Tax Rate (%) | Tax Amount ($) |

|---|---|---|

| First 6,000 Next 59,000 |

0 4 |

0 2,360 |

| First 65,000 Amount exceeding 65,000 |

– 6 |

2,360 |

Example 1: AV of your house is $9,000

| Property Tax payable is: | First $6,000 X 0% | = $ 0 |

| Next $3,000 X 4% | = $120 | |

| Tax payable: | = $120 | |

Example 2: AV of your house is $24,000

| Property Tax payable is: | First $6,000 X 0% | = $ 0 |

| Next $18,000 X 4% | = $720 | |

| Tax payable: | = $720 | |

Example 3: AV of your house is $84,000

| Property Tax payable is: | First $6,000 X 0% | = $ 0 |

| Next $59,000 X 4% | = $2,360 | |

| Remaining $19,000 X 6% | = $1,140 | |

| Tax payable: | = $3,500 | |

The Government announced the introduction of progressive tax rates for all residential properties from 1 Jan 2014 and 1 Jan 2015. See revised rates below.

| Progressive Tax Rates | ||

|---|---|---|

| Annual Value($) | Effective 1 Jan 2014 | Effective 1 Jan 2015 |

| First 30,000 | 10% | 10% |

| Next 15,000 | 11% | 12% |

| Next 15,000 | 13% | 14% |

| Next 15,000 | 15% | 16% |

| Next 15,000 | 17% | 18% |

| AV in excess of $90,000 | 19% | 20% |

| Progressive Tax Rates | ||

|---|---|---|

| Annual Value($) | Effective 1 Jan 2014 | Effective 1 Jan 2015 |

| First 8,000 | 0% | 0% |

| Next 47,000 | 4% | 4% |

| Next 5,000 | 5% | 6% |

| Next 10,000 | 6% | 6% |

| Next 15,000 | 7% | 8% |

| Next 15,000 | 9% | 10% |

| Next 15,000 | 11% | 12% |

| Next 15,000 | 13% | 14% |

| AV in excess of $130,000 | 15% | 16% |

The concessionary tax rates can only be applied to one home owned and occupied by an individual or a married couple. If a married couple were to owner-occupy two homes even though each home is separately owned by each individual and not jointly owned by the couple, the owner-occupier tax rates can only apply to one of the homes.

Only current owners can apply. If you have already sold your property, you can no longer apply.

A residential property owned by a company, association or a body of persons does not qualify for the concession even if its staff lives in its residential property. The owner-occupier tax rates do not apply to non-residential properties or land even if you have bought the properties for your own use/ occupation.

If you and/ or your spouse own more than one home

If you own a residential property (A) and own another residential property (B) with another party other than your spouse (e.g. parents, siblings, etc.)

For HDB or DBSS owners

If you buy a new or resale HDB or DBSS flat, you need not apply for the owner-occupier tax rates as this would automatically apply to your flat as you are required to live in it.

For Private Residential Property (include Executive Condominium)

From 1 Jan 2011, if you buy your first private residential property and do not owner-occupy another home, the owner-occupier tax rates may automatically apply to your private residential property. But if you do not intend to owner-occupy the property, you should inform IRAS immediately, so as to avoid any penalty for late or non-notification.

If you are eligible for the owner-occupier tax rates, but have not been granted owner-occupier tax rates automatically, you may apply for the owner-occupier tax rates.

For partially let homes

If you partially let out your home while still owner-occupying it, you are still eligible for the owner-occupier tax rates. If the owner-occupier tax rates are withdrawn, you may apply for the reinstatement of your owner-occupier tax rates by writing to IRAS to:

[Source: http://www.iras.gov.sg/irasHome/page04.aspx?id=2378]

{kind=link}